10 Things Every New York Family Should Know About College Savings

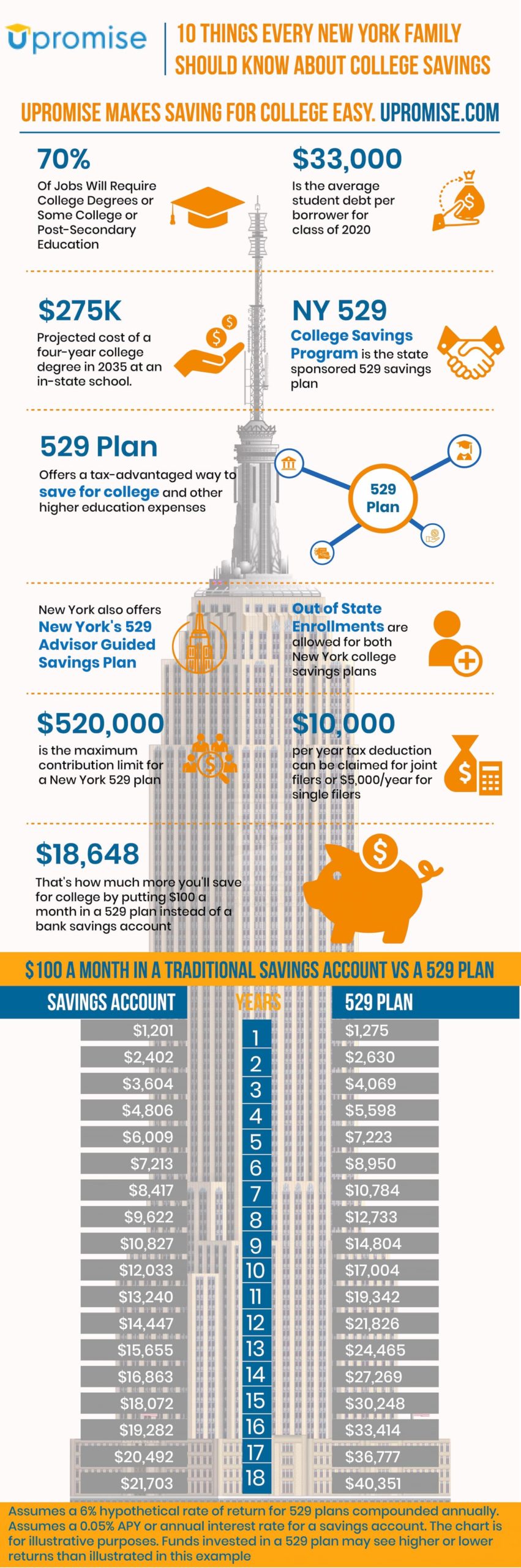

1. By the end of the decade, 70% of jobs will require college degrees or some college or post-secondary education.

2. For the class of 2020, the average student debt per borrower is $33,000.

3. $275K is the projected cost of a four-year college degree in 2035 at a public school in New York state.

4. NY 529 College Savings Program is the state-sponsored 529 college savings plan. This is a direct-sold plan that consumers (family members) can directly enroll in themselves online.

5. 529 plans are a tax advantaged way to save for college.

6. New York also offers another 529 plan: New York’s 529 Advisor Guided Savings Plan. You must enroll in this plan through a qualified financial advisor.

7. Out-of-state enrollments accepted for both of New York’s 529 plans.

8. $520,000 is the maximum contribution limit for New York 529 plans. Contributions may be made to all New York 529 accounts (for the same individual beneficiary) until the balances of all 529 plans reach $520,000. After the plan balances reach $520,000 no additional funds may be put into a plan. (But the funds already invested can continue to grow interest.)

9. $10,00 per year is the max tax deduction that can be claimed for New York state tax filers. $10,000 per year may be claimed for join filers or $5,000 per year for single filers.

10. By putting $100 a month into a 529 plan vs a savings account at the bank, you could make $18,648 more.* The typical 529 plan sees an annual ROI of 6% while the average bank savings account only sees 0.05% in yearly interest.

You can also find more information at nysaves.org. It takes 5-10 minutes to open a NY 529 account online.

New York 529 plan accounts are eligible to be linked to the free Upromise Rewards program. Across the country, Upromise has helped families save over $1 Billion for college. Join free and earn cash rebates and other free cash rewards to save for college and your child’s 529 plan. Additionally, every month 5 Upromise members win a $529 scholarship.

*This assumes a 6% hypothetical rate of return for 529 plans compounded annually and assumes a 0.05% APY or annual interest rate for a savings account. The information in the infographic chart is for illustrative purposes. Funds invested in a 529 plan may see higher or lower rates of return than illustrated in this example.

Here are some common QA’s related to New York state’s 529 plan.

What is a 529 plan?

A 529 plan is a type of account that helps families save for college. The 529 refers to a section of federal tax code that gives this savings program special tax benefits.

Funds that you put in a 529 plan grow similar to how funds grow in a 401(k) plan or other investment accounts. 529 plans are designed to have a higher return on interest than a traditional savings account at the bank.

While money in a savings account at the bank will usually see less than 0.25% in interest every year (less than 1%), funds in a 529 plan can gain 6% interest or more every year.

If you were able to put $1,000 into a NY Saves plan today and just let it sit there, in 10 years you could potentially double your money. You could make nearly $1,000 in interest. In a traditional bank savings account, you would probably only make $25 to $50 in interest.

The ability to see such high returns on your savings in a 529 plan makes this an attractive option for 529 plans.

What are the tax benefits of having a 529 plan?

There are also tax benefits that come with having a 529 plan, both at the federal income tax level and for your New York State income tax deductions.

When the beneficiary (student or child you are saving for) withdraws funds from their 529 plan, they do not have to pay taxes on any of the fund growth or interest as long as the funds go towards qualifying education expenses. This can included tuition for college, trade school or vocational school, graduate school, books, school fees, or room and board. Talk to a tax expert about other eligible post secondary school expenses for federal income tax purposes.

At the state level, there are New York state tax deductions that you can claim for your contributions to your child’s 529 plan NY Saves. Married or joint couples can claim up to $10,000 per year and single filers can claim up to $5,000 per year.

Is a 529 plan FDIC insured?

Some state 529 plans are insured by the FDIC (Federal Deposit Insurance Corporation), but the NY Saves plan is not. Neither the State of New York, nor its agencies (including The Vanguard Group, Inc., Ascensus Broker Dealer Services, LLC), nor any of its affiliates insure NY Saves 529 accounts nor guarantee the principal deposited therein, or any investment returns on any account portfolio.

Funds in a state 529 plan, like funds in a 401(k) plan or other investment portfolio, can lose money. Speak with a qualified financial planner about the best investment and savings options for you.

Does does a 529 plan impact my child’s financial aid?

This is a common concern for many parents, however 529 plan funds generally have minimal impact on a child’s ability to qualify for need-based grants or federal college aid. 529 plan funds are counted as assets of the parents (if the parents opened the account and are the owners) and not of the student’s.

Students are expected to contribute more of their funds to cover their college than parents. With 529 plan funds counted as their parents’ income, a 529 plan account often has little impact on their child’s financial aid.

Additionally, distributions from a 529 plan receive ore favorable treatment on a FAFSA. Qualified distributions (for qualified higher education expenses) are not included in the base-year income calculations that could reduce or limit financial aid eligibility.

Also, in the event your child does not go to college or to post-secondary education, the funds are not forfeited or lost. Those funds don’t go anywhere. They can be transferred, without tax penalty, to a child’s sibling, cousin, or even their future children.

There are many paths to college and to post-high school learning. If a child doesn’t go to college straight after high school, they could resume their post-secondary education ate age 25, 30, or older and the funds will be waiting.

Related Articles:

- Minnesota 529 Plan Basics

- California Plans: 10 Things to Know

- California 529 Plan Basics

- How To Save Money for Your Children’s College Education

- Massachusetts 529 Plan Basics

- Iowa 529 Plan Basics

- Maine 529 Plan Basics

- 10 Things Every California Family Should Know About College Savings

- College Planning Resources for Student Athletes

- West Virginia 529 Plan Basics

- Connecticut 529 Plan Basics

- Kentucky 529 Plan Basics

- How to Get Free Diapers, Formula, and Other Baby Gear

- Are Student Loans Worth It?

All State 529 Plans by State

- Alabama 529 Plan

- Alaska 529 Plan

- Arizona 529 Plan

- Arkansas 529 Plan

- California 529 Plan

- Colorado 529 Plan

- Connecticut 529 Plan

- Delaware 529 Plan

- Florida 529 Plan

- Georgia 529 Plan

- Hawaii 529 Plan

- Idaho 529 Plan

- Illinois 529 Plan

- Indiana 529 Plan

- Iowa 529 Plan

- Kansas 529 Plan

- Kentucky 529 Plan

- Louisiana 529 Plan

- Maine 529 Plan

- Maryland 529 Plan

- Massachusetts 529 Plan

- Michigan 529 Plan

- Minnesota 529 Plan

- Mississippi 529 Plan

- Missouri 529 Plan

- Montana 529 Plan

- Nebraska 529 Plan

- Nevada 529 Plan

- New Hampshire 529 Plan

- New Jersey 529 Plan

- New Mexico 529 Plan

- New York 529 Plan

- North Carolina 529 Plan

- North Dakota 529 Plan

- Ohio 529 Plan

- Oklahoma 529 Plan

- Oregon 529 Plan

- Pennsylvania 529 Plan

- Rhode Island 529 Plan

- South Carolina 529 Plan

- South Dakota 529 Plan

- Tennessee 529 Plan

- Texas 529 Plan

- Utah 529 Plan

- Vermont 529 Plan

- Virginia 529 Plan

- Washington 529 Plan

- Washington DC 529 Plan

- West Virginia 529 Plan

- Wisconsin 529 Plan

- Private College 529 Plan